Institutional Insights: Goldman Sachs "Mega IPO's'

IPO Wave: Large Supply Coming, but History Says Mega IPOs Are Not a Market Problem

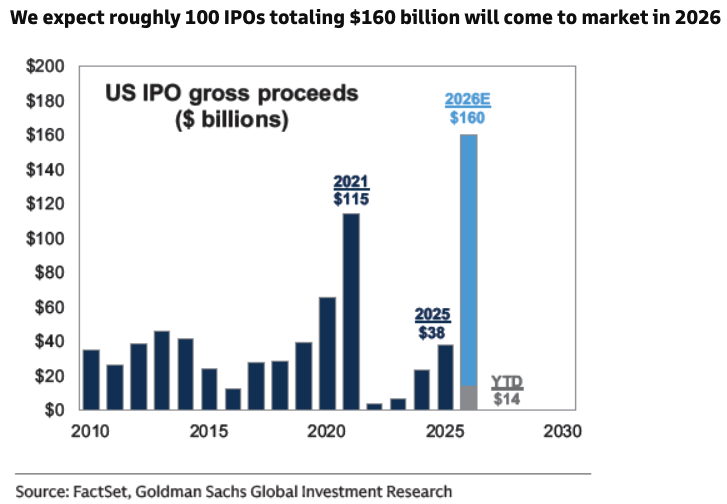

A potential wave of high-profile IPOs is coming back into focus, with Goldman expecting roughly 100 IPOs totaling about USD 160bn to come to market in 2026. That would mark a meaningful reopening of the new-issue market and could include several large, high-profile deals.

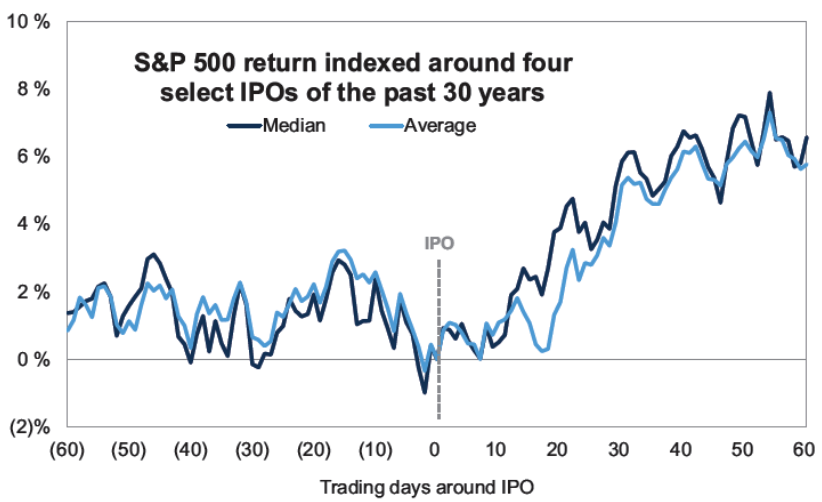

The key conclusion from the historical work is important: mega IPOs do not appear to create broad market pain by themselves. Around the largest historical IPOs — Alibaba, GM, Meta, and Visa — the S&P 500 typically dipped modestly before issuance and then rallied afterward. High-yield credit behaved similarly, suggesting that macro conditions, not IPO supply, were the primary driver of asset-price moves.

In other words, large IPOs may affect liquidity and cash management at the margin, but they have not historically forced broad selling of mega-caps, popular longs, or Momentum.

Key takeaways

Goldman expects roughly 100 IPOs totaling USD 160bn in 2026.

Mega IPOs historically have not caused sustained equity-market weakness.

Around the largest IPOs, the S&P 500 fell about 1% in the month before, then rallied around 5% in the month after.

High-yield credit showed similar behavior, pointing to macro, not IPO supply, as the driver.

There is no clear evidence of forced mega-cap selling or Momentum-factor selling around prior mega IPOs.

Best IPO performers tend to have fast sales growth and a clear path to profitability.

IPOs typically weaken into lockup expiration but recover afterward.

Mutual funds may build cash ahead of large IPOs, but the historical impact has been modest.

Passive index inclusion flows are likely manageable at first, especially when free float is low.

1. IPO calendar: roughly 100 deals and USD 160bn expected in 2026

Goldman expects about 100 IPOs totaling USD 160bn to come to market in 2026.

That would represent a major revival after a quieter IPO environment and would likely be driven by:

improved equity market conditions,

lower volatility,

renewed appetite for growth,

stronger AI and technology demand,

private companies seeking liquidity,

sponsor and venture-backed backlog,

potential high-profile mega IPO candidates.

The broader equity market backdrop is supportive because the S&P 500 is at or near all-time highs, the Vol Panic Index has collapsed, ETF flows remain strong, and investors are rebuilding risk.

The risk is that the market becomes more selective. The IPO window may be open, but investors are likely to distinguish sharply between quality issuers and weaker growth stories.

2. Mega IPOs do not historically create broad market pain

A common concern is that mega IPOs drain liquidity from the market and force investors to sell existing winners to fund allocations. The historical evidence does not strongly support that concern.

Around four of the largest IPOs in the past 30 years — Visa, GM, Alibaba, and Meta — the S&P 500:

declined roughly 1% in the month before the IPO,

then rallied roughly 5% in the month after.

High-yield credit moved similarly around these windows. That is important because HY credit is not directly affected by equity IPO supply in the same way. If both equities and credit behaved similarly, the more likely driver was macro risk appetite rather than IPO-specific funding pressure.

The conclusion:

Mega IPOs are not, by themselves, a reliable bearish catalyst for the equity market.

They may coincide with volatility, but they do not appear to cause lasting market weakness.

3. No evidence of forced mega-cap or Momentum selling

Another concern is that very large IPOs force investors to sell popular longs, mega-cap holdings, or Momentum winners to raise cash.

Goldman’s historical work finds no clear evidence of:

broad mega-cap selling pressure,

forced sales of popular long positions,

systematic Momentum-factor selling,

material pressure on existing index leaders.

That matters for today’s market because many investors are worried that a high-profile IPO — especially a very large technology or space-related deal — could become a source of funds against AI leaders or mega-cap tech.

History suggests that risk may be overstated.

Funding may happen at the margin, but not enough to create a reliable broad market short signal.

4. IPO winners: fast growth and near-term profitability

The best post-IPO performers share a consistent profile:

high sales growth,

improving margins,

near-term path to profitability,

credible business model,

large addressable market,

strong unit economics,

clear use of proceeds,

visible revenue durability.

This is an important shift from the 2020-2021 IPO market, when investors were more willing to fund long-duration growth without profitability.

Today’s public investors appear to prefer companies that combine growth with financial discipline. For IPO candidates, the message is clear: growth is necessary, but not sufficient. The best reception goes to companies that can show a realistic path to profits.

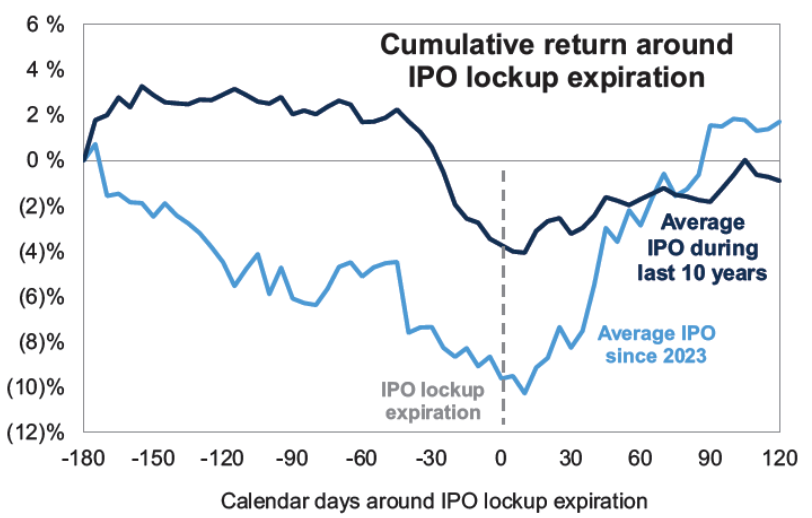

5. Lockups: weakness before expiration, rebound after

Lockup expirations remain a more reliable source of single-name volatility than the IPO itself.

Historical average since 2017

The average IPO since 2017 has declined by roughly 5% during the month before lockup expiration.

After lockup expiration, the stocks typically stabilize and rebound shortly thereafter.

Recent IPOs since 2023

For IPOs since 2023, the pre-lockup pattern has been more pronounced:

average decline of roughly 10% in the six months before the standard 180-day lockup,

but stocks have generally rebounded above their first-day closing price within three months after lockup expiration.

This makes sense. Investors often anticipate insider and sponsor selling before the lockup, pressuring the stock ahead of the event. Once the event passes and supply is absorbed, the overhang clears.

The trading implication:

Lockup weakness can create opportunities, particularly in high-quality IPOs with strong growth and a path to profitability.

6. Mutual funds may build cash, but the effect is modest

Mutual funds often raise cash ahead of very large IPOs, but historically the effect has not been market-disruptive.

Ahead of the four largest IPOs in the last 30 years — Visa, GM, Alibaba, and Meta — each raised roughly 15bps of S&P 500 market cap at the time, equivalent to approximately USD 100bn today.

Mutual-fund cash behavior around those events:

cash rose a median 3% in the prior month,

then fell 2% after the IPO.

Current mutual-fund cash sits at just 1.4% of assets, the 5th percentile over the past 20 years. That is low, meaning funds have room to build cash if large IPOs approach.

In dollar terms, mutual funds hold about USD 181bn in cash, which is around the middle of the range over the past few years.

So yes, mutual funds may raise cash ahead of a major IPO wave. But history suggests this is not enough to create broad market stress.

7. Index inclusion: mechanical selling exists, but initial impact is small

Passive funds can create mechanical reallocation flows when a large IPO is added to major benchmarks. However, fast-tracked large IPOs often enter benchmarks with smaller initial weights because their free float is limited.

Goldman’s example:

A hypothetical company with:

USD 1 trillion total market cap

10% free float

would have a weight of less than 0.5% in the S&P 500.

If passive funds benchmarked to the S&P 500 added that company at benchmark weight, the reallocation would create selling pressure on existing index constituents equal to:

less than 5bps of those constituents’ collective market cap,

less than 5% of their average daily trading volume.

That is manageable.

However, the impact would increase over time as the company’s float factor rises. If insiders, sponsors, or early investors sell and the free float expands, the benchmark weight could grow, requiring additional passive buying of the new stock and selling of existing constituents.

So the first inclusion may be digestible, but later float increases matter.

8. Market implications

IPO supply is not the main risk

The main risk around mega IPOs is not supply itself. History suggests macro drives market outcomes around mega deals.

Important macro drivers include:

rates,

credit spreads,

volatility,

earnings revisions,

liquidity,

geopolitical headlines,

risk appetite,

Fed expectations.

If the market weakens around an IPO, it is more likely because the broader macro tape is deteriorating, not because the IPO is mechanically draining liquidity.

Selectivity will matter

The IPO market will likely reward companies with:

strong revenue growth,

near-term profitability,

credible management teams,

large TAMs,

AI or secular growth exposure,

strong balance sheets.

It will likely punish companies with:

unclear profitability,

weak unit economics,

excessive valuation,

slowing growth,

high cash burn,

heavy insider selling.

Lockup calendars may create better entry points

Rather than shorting the market ahead of mega IPOs, a better strategy may be to watch post-IPO lockup calendars and buy high-quality issuers after pre-lockup weakness.

Passive flow concerns are manageable

Index inclusion can cause mechanical reallocation, but float likely limits initial weights. The bigger passive-flow effect comes later if float increases materially.

Trading takeaway

The IPO reopening is a sign of risk appetite and market health, not automatically a bearish liquidity drain.

The best approach is:

do not short the market simply because mega IPOs are coming,

focus on IPO quality: growth plus profitability,

watch lockup-related weakness for entry opportunities,

monitor mutual-fund cash build, but do not overstate its market impact,

evaluate passive-flow effects based on float, not headline market cap,

watch macro conditions, because macro has historically driven asset moves around mega IPOs.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!