Institutional Insights: UBS Global FX Strategy Month End Perspectives

UBS FX Compass: Month-End FX Still Dominated by Geopolitics

UBS argues that the final week of May remains primarily a geopolitics-driven FX market, with Iran-related headlines still the dominant swing factor. The news mix has been two-sided. On the constructive side, senior officials in both the US and Iran have signalled progress toward a formal understanding that could extend the current ceasefire for a meaningful period, potentially within days. The visit by senior Iranian figures, including the central bank governor, to Qatar is viewed as another important signal, especially because it may point to progress on releasing some frozen Iranian funds as part of a broader deal.

On the negative side, fresh kinetic activity has returned to the Persian Gulf, including exchanges of fire between US and Iranian forces and US attacks on the southern Iranian coast. Israel has also intensified attacks in Lebanon, which could complicate any US-Iran arrangement given Iran’s insistence that a durable ceasefire include Lebanon. Comments from Iran’s new Supreme Leader also underscored continuing hostility toward the US and Israel, including expectations that regional countries remove US bases from their territory.

Despite those negative headlines, UBS notes that price action has remained relatively benign. Markets appear to be assigning higher odds to an eventual ceasefire extension and at least partial Strait of Hormuz reopening, even if the path is messy and headline-driven.

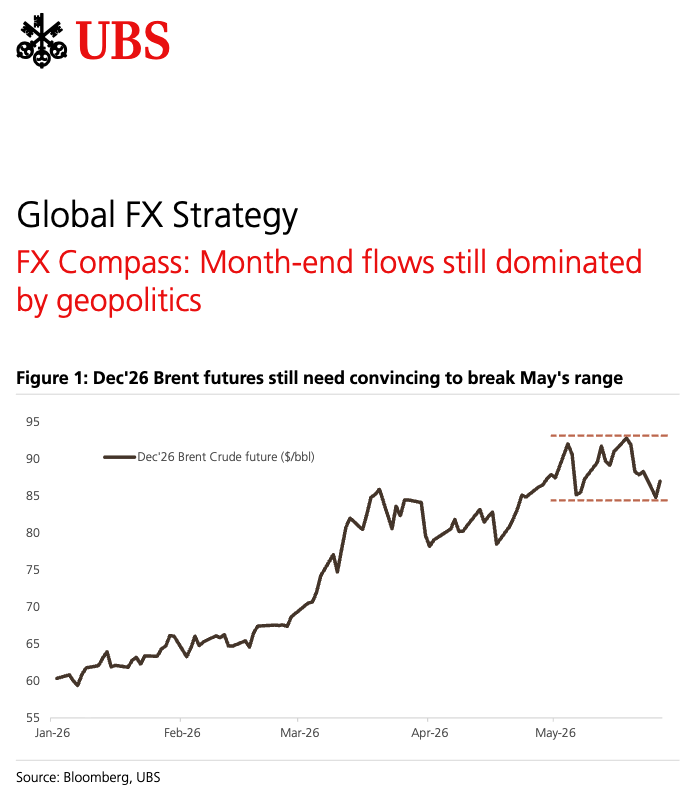

## Oil: Brent futures still need convincing

UBS highlights that Dec 2026 Brent futures are trading around $86/bbl, roughly in the middle of the $82-93 range that has prevailed through May and close to April’s closing level. That is important because it suggests the market has not fully bought into either an extreme escalation scenario or a clean normalization scenario.

The oil market has effectively been expecting some progress toward a ceasefire extension and partial Strait of Hormuz reopening since the April 7 ceasefire announcement. That prior expectation has diluted the price impact of both positive and negative headlines.

UBS also notes that markets are getting used to the idea that there may be no single tipping-point moment where oil shortages create panic. Possible explanations include reduced Chinese demand, increased supply from strategic reserves, and the possibility that Strait of Hormuz blockades are not fully watertight.

The broader theme remains the disconnect between tech-driven equity strength and still-suppressed global energy supply. That disconnect has helped keep risk currencies supported and FX realized and implied volatility low.

## Rates: the more interesting move is the US 10-year washout

UBS finds the recent volatility in the US 10-year yield more interesting than the oil move. Last week, as Dec 2026 Brent pushed toward $93, the US 10-year yield rose to 4.67%, its highest level since January 2025. The 10s-2s spread also widened to 54bps, the widest since March.

Since then, the 10-year yield has fallen back below 4.50%, while the 10s-2s spread has narrowed back toward 42bps, close to the lowest levels since April 2025.

UBS says it is tempting to attribute that move entirely to oil-related news, but the better explanation may be that the long end experienced a positioning washout that has now cleared. If that is right, then one major source of FX volatility has been removed.

That matters because last week UBS had expected the path of least resistance to be toward the stronger-dollar end of its Q2 ranges, such as EUR/USD 1.1450 and AUD/USD 0.7000. Instead, spot has moved closer to UBS’s end-Q2 targets of EUR/USD 1.1600 and AUD/USD 0.7200.

## Fed: not the main driver this week

UBS does not expect US data or Fed speakers to be a clear game changer this week. Investors will still monitor the Fed communication calendar, but the market is already pricing a more open-minded Fed.

UBS notes that Fed Governor Waller, typically seen as dovish, said last week that he is now uncomfortable with the Fed’s easing bias. Meanwhile, markets already price roughly an 80% probability of a 25bp Fed hike by end-2026.

Because the market has already moved toward pricing a Fed that is open to both directions on rates, UBS thinks G10 FX this week is more likely to be driven by Iran-related headlines than by Fed speakers.

The directional FX implication is straightforward: progress toward a deal is likely USD-negative, while setbacks are likely USD-positive.

## Month-end flows: no clear signal, but watch yen selling

UBS updates its month-end FX trading signals model and finds no strong trading signals at this point. However, it has made upgrades to the model to improve accuracy and better capture timing effects around month-end equity rebalancing flows.

One point UBS flags is the possibility that month-end flows could favor JPY selling roughly one day before month-end. This is not presented as a high-conviction signal, but it is a flow risk worth watching given the broader low-vol FX backdrop.

## Key takeaways

UBS’s main message is that FX remains hostage to geopolitics, but the market is not trading as if an extreme oil shock is imminent. Dec 2026 Brent remains in its May range, the long end of the US rates market has calmed after a positioning washout, and risk currencies remain underpinned by the strength of tech-led equities.

For G10 FX, the key impulse remains Iran headlines. A credible ceasefire extension or signs of Strait of Hormuz reopening should be USD-negative and supportive for risk FX. Renewed escalation or breakdown in talks should be USD-positive, especially if it pushes oil and long-end yields higher again.

The month-end flow picture is not sending a strong directional signal, though UBS flags possible JPY selling about one day before month-end. Overall, the market is closer to UBS’s end-Q2 targets than last week’s stronger-dollar scenario, with EUR/USD near 1.1600 and AUD/USD near 0.7200.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!