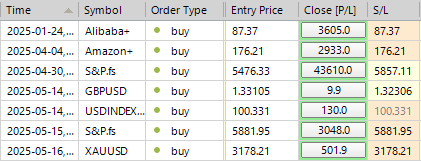

SP500 LDN TRADING UPDATE 19/05/25

SP500 LDN TRADING UPDATE 19/05/25

WEEKLY BULL BEAR ZONE 5860/50

WEEKLY RANGE RES 6049 SUP 5849

DAILY VWAP BULLISH 5928

WEEKLY VWAP BULLISH 5724

DAILY ONE TF UP 5924

WEEKLY ONE TF UP 5805

MONTHLY NEUTRAL

GAP LEVELS 5806

WEEKLY ACTION AREA VIDEO TO FOLLOW AHEAD OF NY OPEN

GOLDMAN SACHS TRADING DESK VIEWS

U.S. EQUITIES COLOR: Weekly Recap

FICC and Equities | 16 May 2025 |

The S&P 500 posted a strong +5% weekly gain, closing up ~1% year-to-date (ytd). Notably, the index is now +19.5% from the April Tariffs Announcement lows, just 50 basis points (bps) shy of entering “bull market” territory. Importantly, the S&P avoided bear market classification, having declined 18.95% peak-to-trough.

Flows Overview:

- Long-only funds (LOs) were net buyers at +$7.5 billion, while hedge funds (HFs) remained balanced.

- Early-week demand, particularly from LOs and sovereign entities, focused on tech/China ADRs and macro plays, driven by favorable trade war developments and an improving inflation backdrop.

- Cyclical sectors outperformed defensives, with much of the buying attributed to short covering as positioning remains low/short.

- Healthcare (HC) saw consistent outsized supply from both LO and HF investors, reflecting ongoing uncertainties and bearish sentiment in the sector.

Derivatives:

- Despite $2.8 trillion in options expiring, this was one of the quieter OPEX sessions recently. Volatility (vol) saw minimal bids as the market gradually climbed ahead of the weekend.

- Flows were muted, though there was some interest in HYG and SPY downside protection in the short-dated space.

- The desk continues to recommend buying short-dated topside as an attractive way to maintain longer delta exposure, given low vol levels and relatively flat dealer gamma positioning.

- Looking ahead, next week will see significant micro focus with key TMT events, including MSFT Build (Mon-Thurs), Dell Tech World (Mon-Thurs), GOOGL I/O (Tues-Wed), and Computex (NVDA, AMD) (Mon-Fri). Illustrating vol compression, next week’s straddle priced at just 1.45%.

Prime Brokerage Trading Flows:

- U.S. equities experienced the largest net buying since December 2021, driven by short covering and, to a lesser extent, long buying (primarily on Monday and Tuesday).

- Hedge funds were likely stopped out during the rally following the U.S.-China trade deal.

- Sentiment in U.S. Energy stocks appears to have bottomed, with hedge funds net buying the sector for a second consecutive week at the fastest pace since September 2022. This week’s notional net buying in U.S. Energy ranks in the 100th percentile of the past five years.

Next Week Outlook:

- The S&P implied move through 5/23 is 1.55%, slightly lower than prior weeks.

- A lighter macro calendar includes Fed speeches and global economic forums (Atlanta Fed Market Conference Mon-Wed, Qatar Economic Forum Tues-Thurs).

- Retail and apparel earnings will be in focus: HD, AS (Tues); LOW, TGT, TJX, VFC, URBN (Wed); ROST, DECK (Thurs).

- TMT events dominate the calendar: SAP Sapphire (Mon-Wed), MSFT Build (Mon-Thurs), Dell Tech World (Mon-Thurs), GOOGL I/O (Tues-Wed), Computex (NVDA, AMD) (Mon-Fri), and STX Investor Day (Thurs).

Sector Highlights:

Technology:

- The Nasdaq 100 (NDX) surged ~6.5% last week, marking its third consecutive close with a 14-day RSI above 70, the most “overbought” level since June 2024.

- Desk flows were skewed toward buying in TMT, with a mix of short covering and long buys. However, by week’s end, debate emerged over whether current positioning and headline momentum can sustain the rally, with revisions likely needing to drive further upside.

- Key events next week include GOOG/MSFT updates and a major Tech/AI conference in Asia (Computex).

Consumer:

- Retail (XRT) jumped +8%, benefiting from trade de-escalation optimism and a second footwear acquisition (SKX followed by FL at an 86% premium).

- While cautious commentary from WMT on pricing and lack of 2Q EPS guidance caused some hesitation, the sector’s low base drove continued long exposure.

- Key focus names: FL deal dynamics, DKS on pullback, TGT, HD, LOW ahead of earnings.

Healthcare:

- Healthcare (XLV) ended the week flat, despite significant daily moves (1%+ every day, 2%+ on four of five days).

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!